Recession, Fed Projections, and the Japanese Carry Trade

Between tariffs shaking borders, a Fed on high alert, and Japan teetering on the edge of a carry trade resurgence, the global economy faces a pivotal week. Will this mark the start of a storm or merely a warning shot for navigators? We unpack the risks and key moves in this analysis.

I. L. R.

3/18/20254 min read

Tariffs, Deficits, and the Atlanta Fed’s Forecasts

After a March dominated by Trump’s tariff agenda, a pivotal week arrives for markets.

On Wednesday, the Federal Reserve will release its economic projections, with all eyes on whether the central bank echoes the warnings from its Atlanta branch. Its GDPNow model has already sent shivers through the room, forecasting a chilling 2.1% contraction for Q1. Will this mark the start of a storm or merely a passing scare?

Meanwhile, alarm bells are ringing in Japan: the trade war is knocking at its door, and inflation has exceeded forecasts for two consecutive months. Could this signal a new chapter for the spectre of carry trade?

For now, a modest cooling in inflation has offered markets a breather, which last week concluded a correction in U.S. indices. The critical question remains: will this correction deepen, or will markets rebound toward growth? Much will depend on the White House’s tone on tariffs and the Fed’s verdict on the domestic economy’s health.

Today on Breaking Bucks , we dissect what Trump’s moves really mean and how to capitalise on the opportunities uncertainty creates in financial markets. Follow us on Twitter for updates.

Recession Risk: The Impact of Tariffs and Trade Retaliation

Does the tariff gamble truly pay off? While the benefits for the domestic economy take years to materialize, retaliation from Canada, Mexico, and China already threatens to erode U.S. output within weeks.

Moreover, the uncertainty generated by Trump clouds the outlook. In this environment, business leaders prefer to wait out the storm before pursuing investments or launching new projects.

However, current tariffs include certain exemptions, leaving room for a short-term deal—however improbable that may seem. This scenario—unlikely as it appears—is the one we’ve consistently argued for at Breaking Bucks since the first round of this trade war.

The potential gains from increased tariff revenues don’t outweigh the risks Trump assumes by alienating trade allies and pushing them toward China.

The key question is whether Canada and Mexico possess the “geoeconomic” sovereignty to challenge the U.S., or if they’ll avoid geopolitical conflict by shying away from closer ties with China.

While this would create a thorny landscape for North American neighbors, it’s equally far from advantageous for the U.S. economy.

Atlanta Fed Forecast Revision: From -2.1% Contraction to GDPNow Model Adjustment

The Atlanta Fed’s GDPNow model—a nowcasting tool that predicts quarterly GDP in real time—initially projected a 2.1% contraction for Q1 2025. Taken out of context, this figure sparked alarm.

However, the plunge stemmed from an unusual factor: a record January trade deficit driven by massive gold imports (192.9 tonnes from Switzerland). Fearing future tariffs, firms accelerated purchases, creating a temporary gold rush.

The technical snag? Gold, unlike goods destined for production or consumption, artificially inflates the deficit and distorts GDP calculations. After adjusting the model to exclude this anomaly, the projection rebounded to +0.4%.

Still, the record January deficit will likely reverse in Q2, with GDP bouncing back as import patterns normalise.

Trade Deficit and Trump’s Economic Strategy: Strategy or Distraction?

While Rubio plays the villain in the U.S.-Russia saga, Treasury Secretary Scott Bessent acts as the firefighter tasked with extinguishing Trump’s verbal blazes. Recently, Bessent followed the White House script, assuring markets there’s “no cause for concern”—provided three conditions are met: “sound fiscal policy, reduced regulation, and energy security.”

The narrative revolves around the trade deficit, as if it were the sole protagonist of this plot. Meanwhile, economic growth has been relegated to a supporting role.

This approach suggests the U.S. economy may soon face a cooling-off period—or perhaps this is all part of the theatre.

Persistent Inflation and the Fed’s Caution

The latest Bureau of Labour Statistics data shows core inflation at 3.1%—a modest dip that seems promising… until you scratch beneath the surface. Shelter, inflation’s Achilles’ heel, remain stubbornly above 0.3% monthly (3.6% annualised), showing no signs of retreat.

As we noted in our prior analysis, the combo of full employment and rising wages continues to pressure service-sector prices. The exception? Services PMIs, which just hit their lowest level since November 2023. Does this signal easing inflation? For now, it’s a reprieve, not a collapse.

Meanwhile, Trump’s strategy to slash energy costs fails to address the structural dilemma. The Fed knows this. Hence, Powell’s March 7 speech made clear there’s no rush to cut interest rates—a polite way of acknowledging the economy remains overheated.

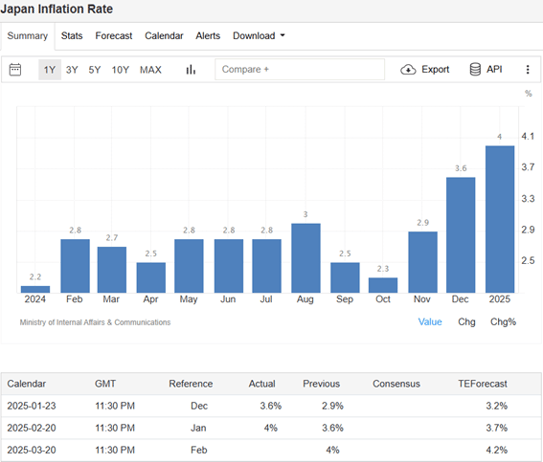

The Japanese Carry Trade Conundrum

This Friday, Japan will release inflation data just a day after the Bank of Japan (BOJ) decides whether to raise interest rates. Spoiler alert: Analysts expect the BOJ to hold rates at 0.5%, maintaining its post-January hike caution. But why such restraint?

The answer lies in Trump’s trade war, which has the BOJ cornered. A rate hike now, combined with tariffs battering Japanese industry, would be like throwing gasoline on a controlled fire. BOJ Deputy Governor Shinichi Uchida put it bluntly: “No rate hikes with unstable markets.”

But here’s the twist: February’s inflation could defy forecasts. Though the yen appreciated in February (typically cooling inflation), projections have already missed in December and January (0.4% and 0.3% margins of error).

If this week’s data significantly exceeds the 4.2% estimate, BOJ Governor Ueda Kazuo might be forced to accelerate his gradual rate-hike plan (target: 2.5% by 2026). This could trigger a domino effect, reviving the dreaded yen-funded carry trade in the U.S.

Outlook and Risks: What Lies Ahead for the Global Economy Amid Uncertainty?

The erratic economic policies of the new administration are breeding uncertainty, undermining business confidence and investment. Shifting tariffs on Canada and Mexico, coupled with unprecedented volatility (the “Political Uncertainty Index” hits historic highs), are stifling growth, fuelling inflation, and discouraging hiring and capital expenditure.

With stubborn inflation and a runaway deficit, the pressure in the pot keeps rising. Japan’s inflation spiral is just one front that could trigger a chain reaction, dragging markets into the abyss.

At Breaking Bucks , we believe Trump will seek a deal with Canada and Mexico to ease tensions. The critical question now is whether he’s willing to slow the economy short-term to rebuild it with less reliance on public spending and trade deficits.

As China follows the U.S. playbook, repairing the plane mid-flight seems the only option. Will it work? Only time will tell. For now, markets hold their breath.