Innovative Industrial Properties (IIPR): The Cannabis "Landlord" Cultivating Dividends

IIPR: A 12% Dividend Yield and Undervalued Assets in the Volatile Medical Cannabis Sector – Time to Bet on a Recovery?

I. L. R.

4/1/20253 min read

Innovative Industrial Properties (IIPR): The Cannabis "Landlord" Cultivating Dividends

In the chaotic ecosystem of the US cannabis industry—where companies grow flowers but harvest losses—IIPR stands out as a strategic outsider: it doesn’t plant seeds but instead leases greenhouses.

As a real estate investment trust (REIT) specialising in cannabis infrastructure, its model is as simple as it is brilliant. IIPR acquires key properties—from cultivation facilities to processing plants—and rents them to producers under triple-net leases. This shifts operational risks to tenants, who often prefer paying premium rents over taking on debt.

Why? Stifling federal legislation leaves cannabis operators with prohibitively high interest rates on loans, making IIPR’s model a lifeline.

Today on Breaking Bucks, we’re dissecting whether IIPR presents a viable investment opportunity. Follow us on Twitter for updates.

IIPR: Stagnant Growth or Latent Opportunity?

IIPR generates $310 usd million annually, with flat growth in a sector projecting a 10% CAGR through to 2030 (and 15% growth already recorded in 2024). While the company isn’t expanding, as the only listed REIT exclusively specialising in cannabis, it holds a unique advantage: waiting for prime sale-and-leaseback opportunities at attractive prices, with few competitors in the market.

The appeal of IIPR isn’t rooted in growth expectations but in its competitive moat and undervaluation.

IIPR’s Double-Edged Sword: Liquidity vs. Tenants in Intensive Care

Cannabis producers, suffocated by regulations, can’t access traditional financing. Here, IIPR steps in as their “liquidity dealer” via sale-and-leaseback deals. But this model cuts both ways:

Tenants with balance sheets greener than their crops: In 2023, 30% of U.S. cannabis operators reported operating losses, with recurrent rent defaults.

Replacement lag: If a tenant collapses, IIPR may take months to find a replacement.

IIPR Under the Microscope

The leadership team isn’t a group of novices—they bring decades of real estate expertise. Their financial discipline speaks for itself:

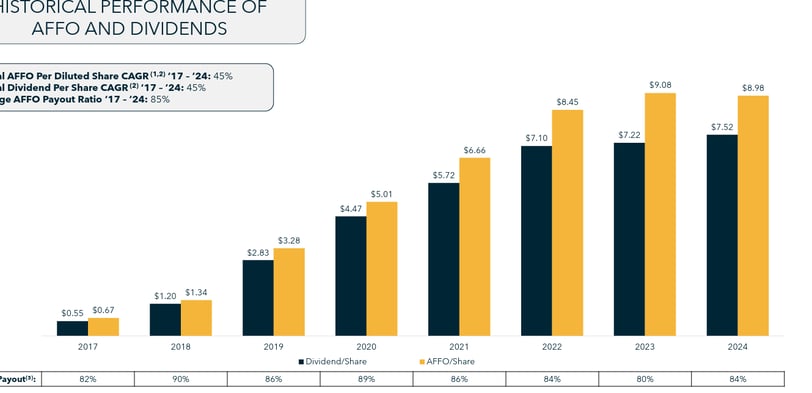

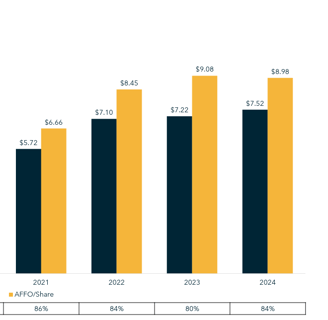

Controlled debt : Only 11% of assets are leveraged (2x net profit), a commendable discipline.

Robust AFFO : 16% free AFFO after dividends, providing a buffer for storms—though not indefinitely.

Discounted valuation : A $1.8 billion market cap (vs. $2.5 billion in assets) and a price-to-book ratio below 1 signal a potential bargain.

Historically, buying below book value has proven lucrative, provided management navigates crises. IIPR’s track record here is strong: swift property reclamation and tenant replacement, as seen in past defaults.

The Perfect Storm: PharmaCann and Other Troubled Tenants

PharmaCann, IIPR’s largest tenant (16.3% of revenue), defaulted in December 2023. A January agreement hinged on a loan that never materialised.

Worse, three more tenants—contributing 10.8% of revenue—have also defaulted. For a firm accustomed to annual hiccups, this is a severe stress test.

Why Stay Calm?

Despite headwinds, IIPR’s valuation already prices in significant risk. At $54 per share (vs. $9 annual AFFO), its 6x P/AFFO ratio looks tempting in a 10%-growth sector. If IIPR weathers the storm (and its history suggests it can), a return to pre-crisis highs above $100 isn’t unthinkable.

Even in a worst-case scenario, the dividend—though potentially trimmed by 30%—would still yield 8.4%.

The Wildcard: DEA Reclassification

A pivotal external catalyst looms: the DEA’s potential reclassification of cannabis from Schedule I to a less restrictive category. This move, under review since 2023, would dismantle regulatory barriers and supercharge demand for specialised infrastructure—core to IIPR’s business.

Bipartisan support, from reform advocate Robert F. Kennedy Jr. to Trump’s pro-legalisation stance in Florida, hints at shifting political winds.

Asymmetric Risk-Reward

IIPR isn’t for the faint-hearted: recent defaults are real, and stability won’t come overnight. Yet its discount to book value, proven resilience, and regulatory tailwinds sketch a scenario where risk-reward tilts in favour of patient investors.

For those bullish on cannabis’s long-term prospects, IIPR could be a classic “buy low, sell high” play.